The technology is ready for an industrial block

Circulera is a science-led manufacturing company for PHA/PHB materials. The work is not a packaging label. It is a production programme: strains, fermentation, recovery, QA, compounding, product recipes, pilot production and end-of-life validation.

Circulera produces PHA, not PLA. PLA appears on this page because it is the current "eco plastic" benchmark: many producers make it, many buyers recognise it and many procurement teams assume compostable means solved. That assumption is the problem.

The next gate is commercial. Circulera is ready to anchor up to $150M into staged GCC manufacturing. To start the first production block, the project needs 3,000 t/y of offtake from buyers who want single-use packaging that can follow the food-waste route instead of becoming permanent plastic.

Technology:

strains, fermentation know-how, recovery route, pilot production and SKU validation.

First block:

PHA resin plant first, finished-goods conversion after buyer offtake and RFQ.

Commercial gate:

3,000 t/y offtake unlocks the first build decision.

Why this matters

Single-use packaging for food should not need a separate, expensive afterlife. The cup or tray is already contaminated with food. If the material can travel with food waste into composting or anaerobic digestion logic, the municipality can reduce sorting, washing, rejected streams and long-lived leakage.

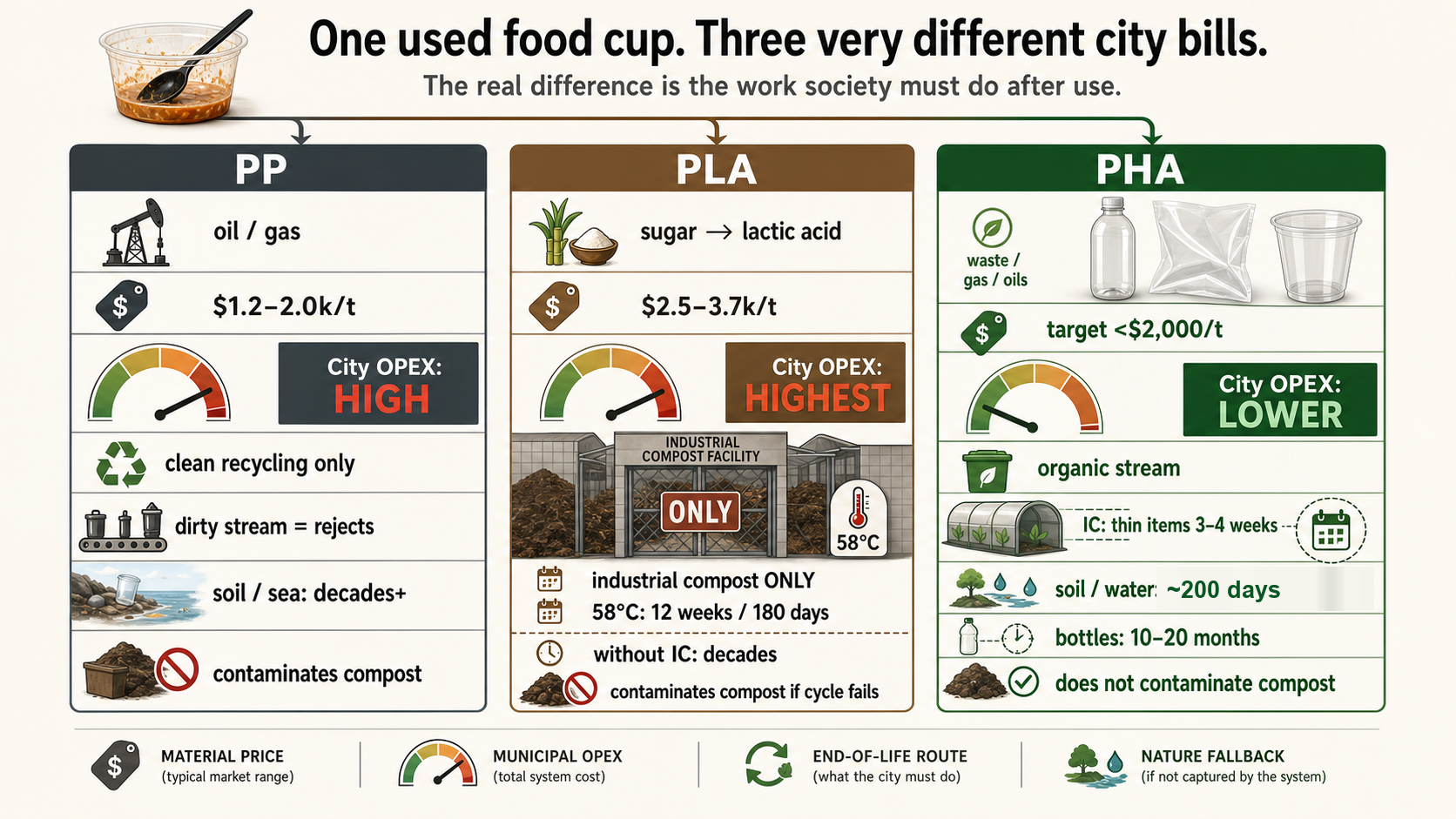

PHA is built for that thesis. It is a bacterial storage polymer family that microbial environments can use as carbon. PLA is different: it can work, but only when the city or operator provides the right hot industrial composting system, enough time, clean collection and contamination control.

Municipal cost:

less need for separate PLA-only bins, education, logistics and reject management.

Waste value:

food residue plus validated PHA formats can support compost or biogas routes.

Product need:

cups, lids, films, bags, bottles, trays, coatings and selected medical P4HB formats.

Public story:

countries can explain an industrial solution, not another green packaging slogan.

See PHA disappear in time-lapse

Why we compare PHA with PLA

PLA is not the product. It is the benchmark Circulera has to beat because the market already treats PLA as the familiar ecological option. PLA is not useless; it is infrastructure-dependent. EN 13432 industrial composting requires disintegration within 12 weeks and biodegradation within six months. That means heat, time, aeration, moisture and operator acceptance. For a food-service cup, that is often the expensive part.

On-site food digesters and short organic cycles are designed for food waste, not for a PLA cup that needs a controlled hot compost route. The practical question for cities is therefore not "is PLA certified somewhere?" but "who pays to collect, heat, aerate, moisturise, monitor and sort this packaging here?"

PLA route:

useful where separate collection and industrial composting actually exist.

PHA route:

stronger where packaging is food-contaminated and should follow organic waste.

TCO route:

compare material price plus bins, sorting, logistics, heat, rejects and fallback.

The market wave has started

Biobased plastics capacity is still tiny versus global plastics, but it is scaling. European Bioplastics reports global biobased plastics capacity growing from 2.31M t in 2025 to about 4.69M t by 2030, with PHA among the polymer families behind the growth.

China is also moving from standards to capacity. GB/T 41010-2021 sets degradability and labelling requirements for biodegradable plastics and products. Bluepha publicly states a PHA site in Yancheng and continued capacity expansion plans. Chinese media reported in April 2026 that Micro Factory / MyPHA completed a 10,000 t/y PHA line, after a 1,000 t/y flexible manufacturing line and a planned 30,000 t/y base.

Regulation pull:

SUP bans, EPR, procurement rules and plastic taxes keep pushing buyers away from permanent SUP.

Capacity signal:

China is industrialising PHA, not just researching it.

Packaging demand:

food, delivery, retail, aviation and hospitality need credible single-use replacements.

Timing:

regional first movers can secure feedstock, sites, buyers and standards before capacity becomes commodity.

Why GCC and Middle East can win

China has scale. The GCC has a different advantage: local organic streams, date-processing by-products, industrial zones, ports, capital, seawater/brine context, energy infrastructure, a strong public sustainability agenda and fast-moving single-use plastic policy. That combination can make local PHA manufacturing more valuable than importing another resin.

Local carbon:

date streams, food waste, gas-route options and regional biomass logic.

Industrial base:

utilities, ports, zones, warehouses and export corridors.

Water context:

seawater and brine are not side notes; they shape site and process choices.

Public value:

lower municipal burden, local jobs, biotechnology capability and exportable products.

First production block

The architecture is staged. Stage 1 starts with one 320 m3 fermenter and a practical industrial footprint, then expands into a larger PHA resin block and separate finished-goods conversion for HoReCa, retail, aviation and industrial buyers.

PHA resin plant:

one 320 m3 fermenter, about 1,725 t/y PHA pellets, 400 kW and a practical 4,000-6,000 m2 plot.

Finished goods:

film, bags, cups, bottles, trays and containers follow offtake and vendor RFQs.

Regional platform:

GCC production with local feedstock, industrial base and regional export.

Cost curve and TCO

PHA is expensive today because fermentation, feedstock and downstream recovery are expensive. Current industrial PHA is about $3,700-4,100/t and is not subject to plastic tax. The goal is to move down the cost curve through scale, better strains, local feedstock and simpler recovery.

PHA does not have to beat PP on resin price alone. It competes on total system cost: EPR, disposal fees, plastic taxes, sorting, composting infrastructure, carbon data, procurement rules and reputation.

PP:

$1.2-2.0k/t resin before taxes and end-of-life costs.

PLA:

$2.5-3.7k/t before the infrastructure burden.

PHA:

$3.7-4.1k/t today, with no plastic tax exposure.

System cost:

PHA targets the municipal bill, not only the resin invoice.

Product direction

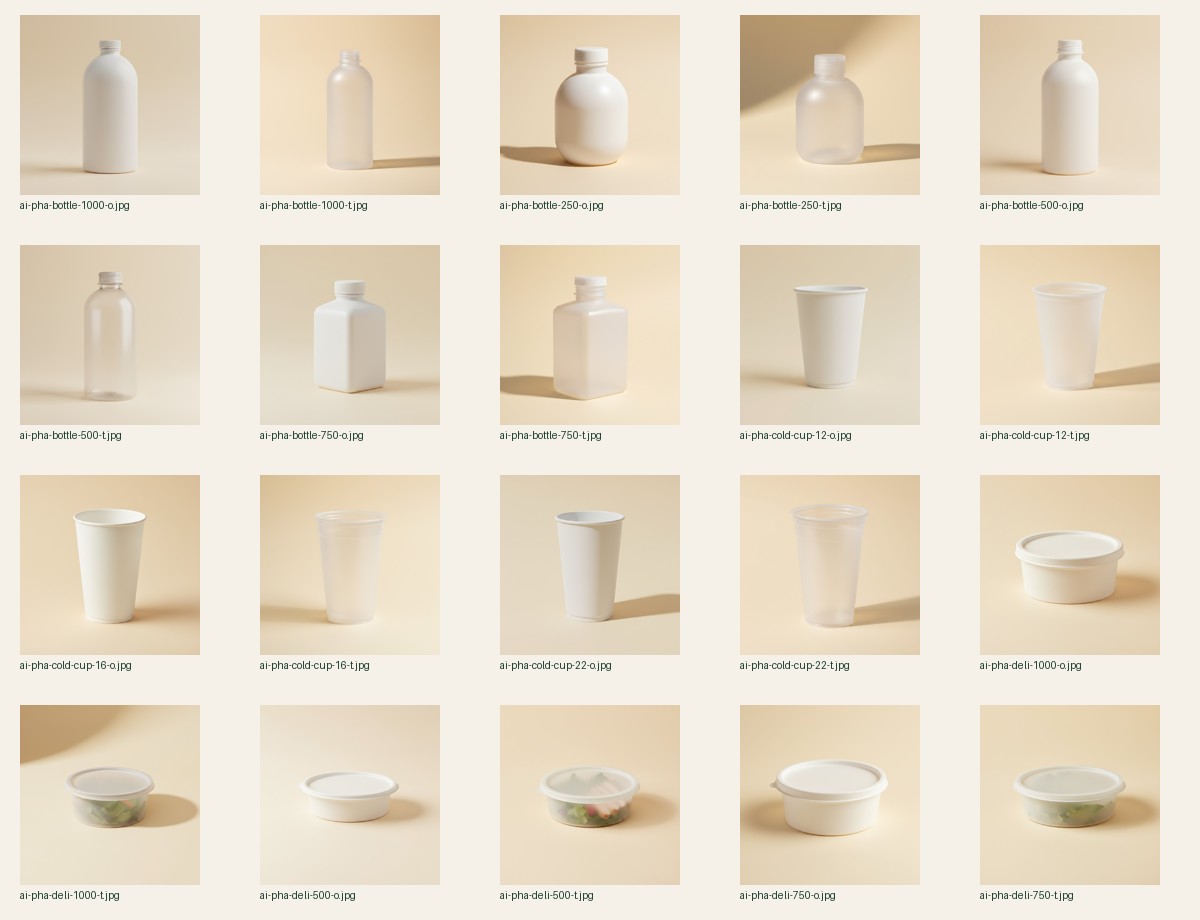

The production direction is visible in the catalogue: resin, PHA-coated paper, PHA/PBAT formats, bags, films, bottles, cups, trays, selected medical P4HB and a bagasse trading line for buyers who need it.

Sources

- European Bioplastics, 2025 market data update: global biobased plastics capacity is projected to rise from 2.31M t in 2025 to about 4.69M t by 2030.

- European Bioplastics on EN 13432: industrial compostable plastics must disintegrate after 12 weeks and biodegrade after six months.

- EU Single-Use Plastics Directive 2019/904: official EUR-Lex text.

- China GB/T 41010-2021: official standard record for degradability and identification requirements of biodegradable plastics and products.

- Bluepha: public PHA capacity and expansion statement.

- Sina Finance, April 2026: reported completion of China's first 10,000 t/y PHA line by Micro Factory / MyPHA.